Taxes and social security contributions for autónomos in Spain

The taxes and social security contributions for autónomos in Spain break into three main blocks that together weigh between 25% and 45% of turnover depending on activity level. The monthly social security cuota, the IRPF (progressive income tax) and the IVA (VAT) form the heart of the self-employed worker's taxation. On top, strict quarterly accounting obligations leave no room for delay.

This article explains exactly how much you will pay as an autónomo in Spain depending on your income level, how the three main taxes are calculated, when each modelo (303, 130, 100, 390) must be filed, how to optimise your tax burden legally via deductions, and which pitfalls to avoid in order not to accumulate debts or penalties.

What are the three big taxes that hit an autónomo?

Before going into the detail, here is the overall picture of autónomo taxation.

The IRPF, progressive income tax

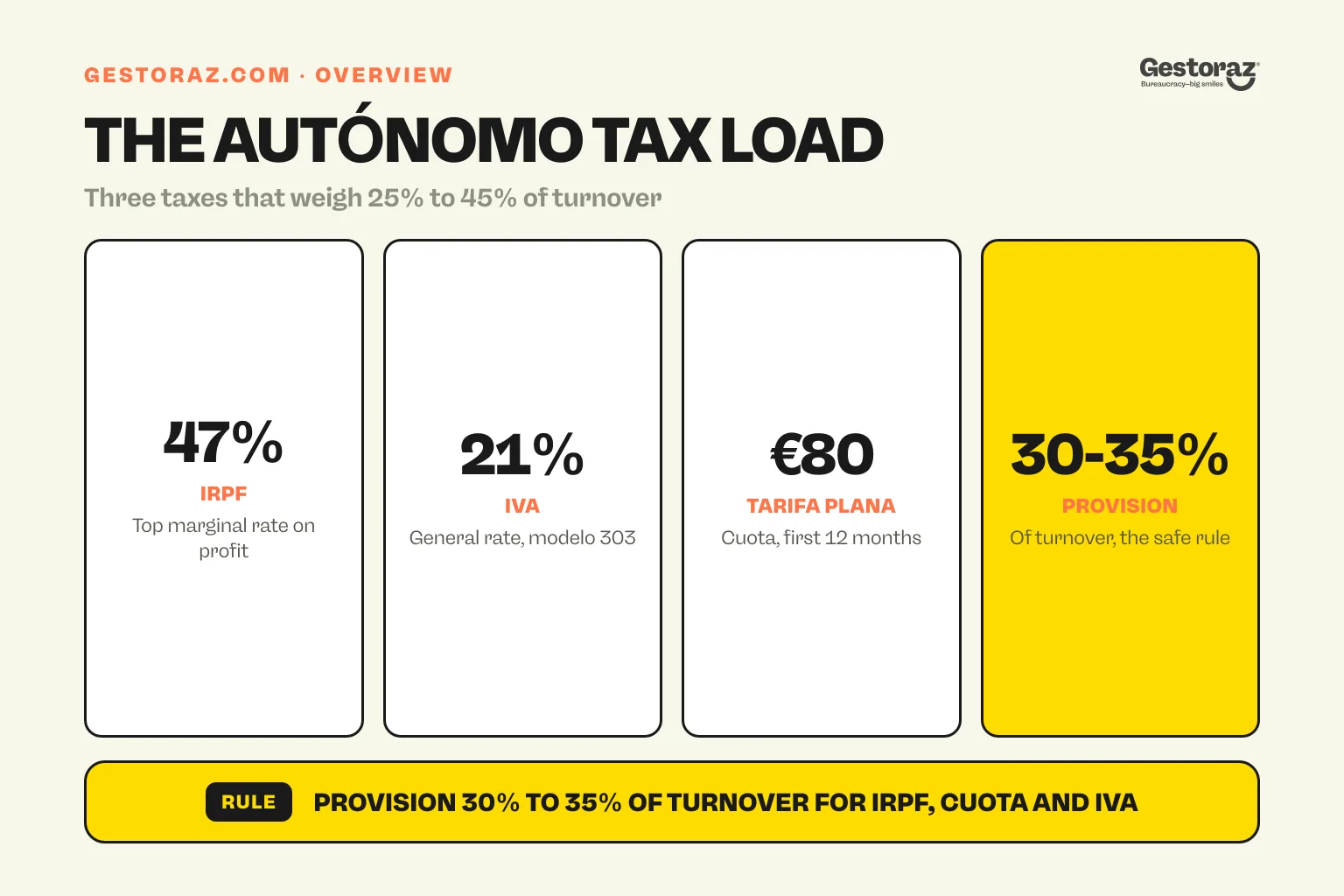

The IRPF (Impuesto sobre la Renta de las Personas Físicas) is the personal income tax. For the autónomo, it applies on profit (income minus deductible expenses) according to a progressive scale that can reach 47% at the margin. It is the main fiscal lever and the one that depends most on income level.

The IVA, VAT collected and deductible

The IVA (Impuesto sobre el Valor Añadido) is not an economic cost for the autónomo: you collect it on your invoices and you deduct it from your professional purchases. The balance is paid to the Agencia Tributaria via the quarterly modelo 303. But IVA weighs on your cash flow between collection and remittance.

The monthly social security cuota (RETA)

The cuota is the monthly flat fee paid to the TGSS under the Special Regime for Self-Employed Workers (RETA). It funds your public healthcare, pension and sickness/unemployment benefits. Since 2023, it is calculated by tramos based on your projected net income. To understand the full system, see how the Spanish social security system works.

How does the IRPF work for autónomos?

IRPF is the main tax on personal income and applies to the net profit of the activity.

Net profit calculation

Net profit = net turnover − deductible expenses. Expenses include equipment purchases, office rent or the share of your home if you telework, software subscriptions, travel costs, gestoría fees, professional insurance, and depreciation (equipment > €300).

The direct estimation regime

Most autónomos are under direct estimation (simplified or standard depending on turnover). Under simplified direct estimation (turnover < €600,000), you deduct your actual expenses plus a flat 5% allowance (max €2,000) for hard-to-justify costs. It is the most advantageous regime for most freelancers.

The progressive IRPF scale 2025

IRPF applies under a national scale to which a regional scale is added (slightly different by autonomous community). For 2025, the average combined scale is:

- Up to €12,450: 19%.

- €12,450 to €20,200: 24%.

- €20,200 to €35,200: 30%.

- €35,200 to €60,000: 37%.

- €60,000 to €300,000: 45%.

- Above €300,000: 47%.

IRPF withholdings on invoices

If you invoice Spanish companies, your invoices carry an IRPF withholding (15% generally, 7% in the early years). This withholding is paid by your client to the Agencia Tributaria via their own modelo 111 and counts as an advance on your annual IRPF. For the detail of rates and exemptions, see when an autónomo uses IRPF withholding.

How does IVA work for autónomos?

IVA is a tax to manage rather than to pay economically, but it requires administrative rigour.

IVA rates in Spain

Three main rates: 21% (general rate, professional services, electronics, clothing), 10% (reduced rate, hospitality, transport, new property), 4% (super-reduced rate, basic food, books, medication). To check the rate applicable to your activity, see check which VAT rate applies in 2025.

IVA balance calculation

Balance to pay = IVA collected on sales − IVA deductible on professional purchases. If the balance is positive, you pay the difference to the Agencia Tributaria. If negative (more purchases than sales, for example at activity start), you carry the credit to the next quarter or request an annual refund.

IVA exemptions

Some activities are IVA-exempt: medical and paramedical services (except aesthetics), regulated education, financial and insurance services, residential housing rentals. If your activity is exempt, you do not invoice IVA and you do not deduct IVA from your purchases.

Simplified regime and modules

Some activities can opt for the simplified regime or modules regime (flat estimation) which simplifies returns. It is mainly used by craftspeople and some neighbourhood shops. For most freelancers and consultants, the general regime is mandatory.

How much does the monthly social security cuota cost?

The cuota depends on your projected net income and varies across 12 tramos.

Contribution tramos 2024-2025

Since 2023, the cuota follows a progressive grid:

| Net monthly income | Monthly cuota |

|---|---|

| Up to €670 | €230 |

| €670 to €900 | €230 |

| €900 to €1,166 | €260 |

| €1,166 to €1,300 | €291 |

| €1,300 to €1,700 | €294 |

| €1,700 to €1,850 | €350 |

| €1,850 to €2,030 | €370 |

| €2,030 to €2,330 | €390 |

| €2,330 to €2,760 | €415 |

| €2,760 to €3,190 | €440 |

| €3,190 to €3,620 | €470 |

| Above €6,000 | €590 |

The Tarifa Plana at €80

New autónomos (or those who have not been registered for 2 years) benefit from the Tarifa Plana: €80/month for the first 12 months. If your income stays under €1,166/month, the Tarifa Plana is extendable for 12 more months. Total possible saving: ~€2,500-€5,000 over 1 or 2 years.

Annual regularisation

The tramo chosen at the start of the year is adjusted in N+1 based on actual income declared in IRPF. If you underestimated, the TGSS bills you the difference; if you overestimated, you get a credit. This protects against poorly calibrated conservative or optimistic choices.

What the cuota gives you

In return, you access: public healthcare via TSI (see the Spanish healthcare system), pension (calculated on your contribution years), sickness benefits, maternity/paternity leave (16 weeks at 100%), and unemployment benefits (since the recent improvement of the regime).

What fiscal calendar should you respect as an autónomo?

The autónomo has a structured annual calendar that is best automated or delegated to a gestoría.

Quarterly returns

Four times a year, the autónomo files:

- Modelo 303 (IVA collected and deductible): before the 20th of the month following each quarter (April, July, October, January).

- Modelo 130 (IRPF instalment): same dates if you are not subject to client withholdings at source.

- Modelo 111 (IRPF withholdings on invoices from professionals you pay): only if you pay subcontractors with withholding.

- Modelo 349 (intra-EU summary): if you do B2B operations with other EU countries.

Annual returns

Annually, you file:

- Modelo 100 (IRPF return): between April and June for the previous year. It is the reference return that consolidates all your income.

- Modelo 390 (annual IVA summary): before 30 January for the past year.

- Modelo 190 (annual IRPF withholding summary): before 31 January.

- Modelo 720 (foreign assets > €50,000): before 31 March, if applicable.

Monthly TGSS cuota

The cuota is automatically debited by the TGSS from your bank account on the last working day of each month. Check that your account is sufficiently funded to avoid rejections and penalties.

Practical advice

Note the dates in your calendar at least 5 days ahead. Better: automate via a gestoría that prepares and submits your returns on time. For €60-€150/month, you avoid oversights that can cost several hundred euros in penalties.

What deductions can an autónomo claim?

Deductions are the main optimisation lever to reduce IRPF.

Costs directly linked to the activity

- Office rent or share of housing (by m² allocated to the activity, generally 20-30%).

- Suministros (electricity, water, gas, internet) up to 30% of the share allocated to the activity.

- Phone and professional subscriptions at 100% if exclusively professional.

- Equipment: depreciation spread over 4-10 years depending on nature.

- Software and SaaS subscriptions: 100% deductible.

Travel costs

- Professional travel: transport, accommodation, meals (with supporting documents).

- Vehicle: deductible only if exclusively professional (rare in practice). For mixed use, deduction possible on actual costs with justification.

Fees and services

- Gestoría and accountant: 100% deductible.

- Lawyer, notary, advisor: deductible if linked to the activity.

- Professional insurance: deductible.

- Professional training: deductible.

Autónomo cuota

Your monthly cuota paid to the TGSS is fully deductible from your activity income. It is one of the main deductions and applies automatically.

Individual pension plan

Contributions to a pension plan give a tax reduction up to €1,500 per year (since the 2022 reform that lowered the cap).

Worked example: autónomo in year one with Tarifa Plana

To make all this concrete, take a typical case.

Profile and figures

A freelance consultant starts in January 2026 with €30,000 of net turnover on the year. He has €5,000 of deductible expenses (equipment €1,200, gestoría €1,500, subscriptions €800, housing share €1,500) and benefits from the Tarifa Plana all year.

Calculations

- Fiscal profit: €30,000 − €5,000 − €960 (Tarifa Plana cuota × 12 months) = €24,040.

- Estimated IRPF (with personal allowances): ~€4,200.

- Tarifa Plana cuota: €80 × 12 = €960.

- IVA: not quantified here (collection and remittance roughly balanced).

- Total social and fiscal cost: ~€5,160, or 17% of turnover.

In year two without Tarifa Plana

Same numbers but standard cuota (tramo €350 × 12 = €4,200):

- Total social and fiscal cost: ~€8,400, or 28% of turnover.

The jump between year 1 and year 2 is significant and must be anticipated in cash flow.

What pitfalls should autónomos avoid?

Several mistakes recur and prove costly.

Underestimating the cuota after the Tarifa Plana

Many new autónomos do not provision for the cuota increase that follows the Tarifa Plana. The jump from €80 to €350-€590/month creates a cash flow hole in year 2. Provision from year 1.

Forgetting IRPF withholdings on invoices

If you invoice Spanish companies, your invoices must carry the IRPF withholding (15% generally, 7% in the first years). Without the mention, the client withholds anyway but your invoice is rejected by their accounting. For details, see when an autónomo uses IRPF withholding.

Poorly separating professional and personal accounts

Keeping a mixed bank account (pro + personal) hugely complicates fiscal justification. Open a dedicated account for the activity from the start, it is non-negotiable for clean accounting.

Forgetting modelo 349 for EU operations

If you invoice companies in other EU countries, you must register with the ROI (Registro de Operadores Intracomunitarios) and file the quarterly modelo 349. Without ROI, you wrongly invoice Spanish VAT and your EU clients refuse the invoices.

Not anticipating the switch to SL

Above ~€50,000-€60,000 of annual profit, switching to a Sociedad Limitada becomes fiscally advantageous. To compare, see autónomo vs SL in Spain and the step-by-step guide to setting up an SL.

Confusing direct estimation and modules

The modules regime is attractive on paper but reserved for some activities (crafts, small shops). For most freelancers, direct estimation is mandatory. Check your eligibility before choosing.

Where to start managing your autónomo taxation

The taxes and social security contributions for autónomos in Spain form a structured but demanding set, requiring rigour in the calendar (quarterly + annual returns) and finesse in deductions. Well managed, the autónomo status can be very favourable up to €50,000 of annual profit; above that, the switch to SL often becomes more advantageous. The full step-by-step launch path sits in how to become an autónomo in Spain.

The practical rule: provision 30-35% of your turnover to cover IRPF + cuota + IVA on average, automate quarterly returns via a gestoría, fully use the Tarifa Plana in year one, and keep clean accounts from the first euro invoiced. Bad management can lead to social and fiscal debts taking years to regularise.

Are you starting as an autónomo or do you want to structure your taxation to optimise deductions? At gestoraz, we can manage the full calendar (303, 130, 100, 390, 190) for €60-€150/month, identify forgotten deductions, and advise you on the threshold to switch to an SL.

Official sources

- Agencia Tributaria, autónomos, sede.agenciatributaria.gob.es: modelos 303, 130, 100, 390, 111, 190, 349 and instructions.

- Tesorería General de la Seguridad Social, sede.seg-social.gob.es: autónomo contribution tramos and Tarifa Plana.

- Ley 35/2006 IRPF (BOE), boe.es/buscar/act.php?id=BOE-A-2006-20764: reference text on IRPF.

- Ley 37/1992 IVA (BOE), boe.es/buscar/act.php?id=BOE-A-1992-28740: reference text on VAT.

- Real Decreto-ley 13/2022 (BOE), boe.es/buscar/act.php?id=BOE-A-2022-12482: new contribution system by tramos.

- Ley 20/2007 del Estatuto del Trabajo Autónomo (BOE), boe.es/buscar/act.php?id=BOE-A-2007-13409: legal status of the autónomo.

Obtain your Digital Certificate entirely remotely.

Request your Digital Certificate completely remotely.