The impact of your NIE on your tax status in Spain

The impact of the NIE on your tax status in Spain is a widely misunderstood topic. Many foreigners believe that holding an NIE automatically makes them Spanish tax residents, or conversely that an NIE protects them from any Spanish taxation. Both claims are wrong. The NIE is a neutral administrative identifier: it does not change your tax status, it simply identifies you to the Agencia Tributaria for the filings that actually concern you.

This article explains exactly what your NIE triggers fiscally (nothing automatic), what it allows (filing the right returns based on your real status), and how your true tax status is determined alongside the NIE (by days of presence, centre of economic interests, family). We detail the fiscal consequences depending on whether you are a non-resident owner, an employee becoming resident, an autónomo, or an heir.

What does the NIE change about your fiscal situation?

Short answer: nothing automatic. But the NIE conditions what you can and must declare.

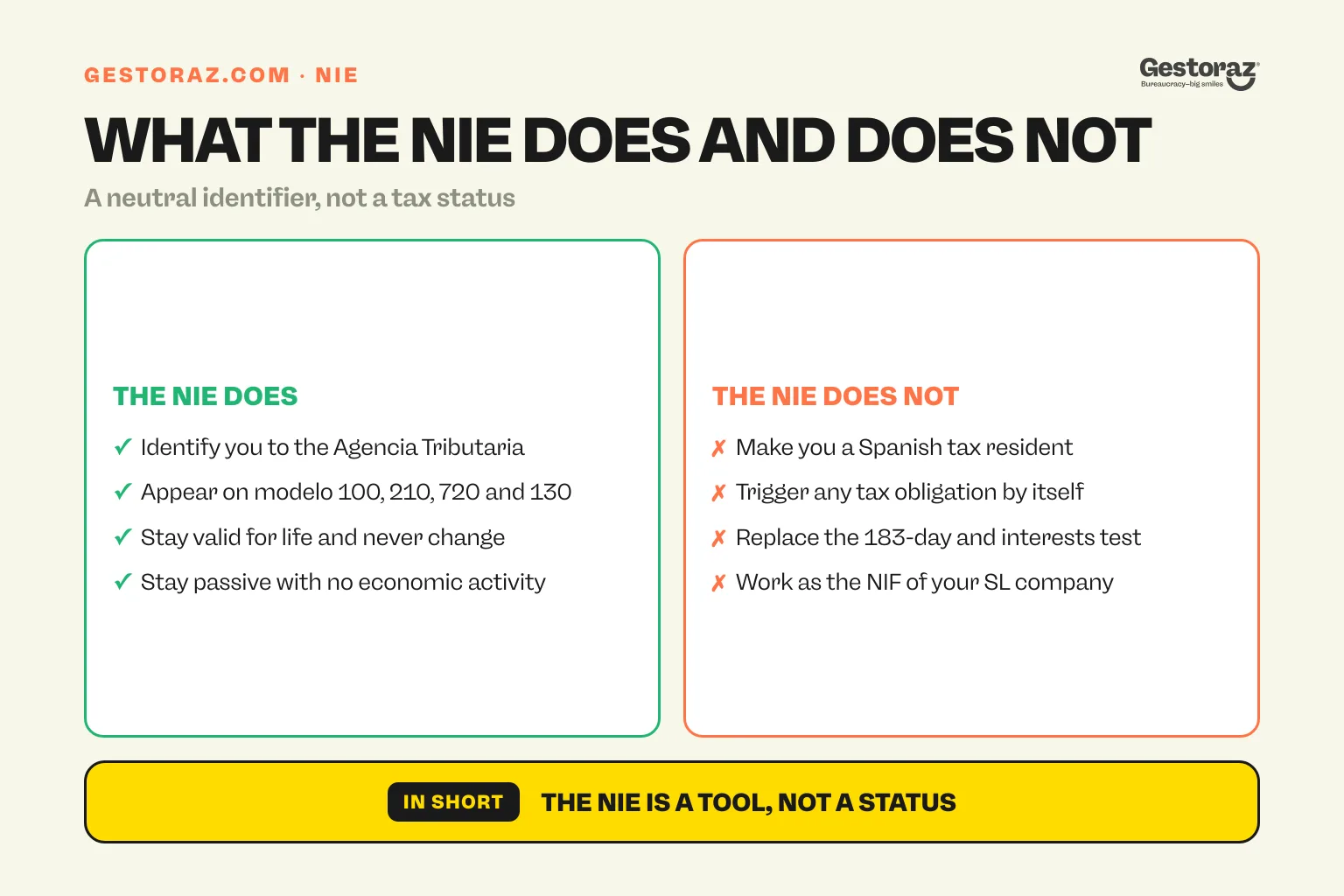

The NIE triggers no tax obligation in itself

Holding an NIE does not make you liable for taxes in Spain. It is your activity or your physical presence that triggers obligations: you pay IBI because you own property, IRNR because you rent out an apartment, IRPF because you become a tax resident. The NIE is just the identifier used to file those returns, like a registration number. To understand the identifier itself, see the NIE in Spain and how long it takes to apply for an NIE.

The NIE lets the Agencia Tributaria know you

Once your NIE is allocated, you appear in the Spanish tax database. If the administration spots that you own property (via the notarial deed), it will expect a modelo 210 every year. If you sign a Spanish employment contract, it will expect an IRPF return. The NIE is what links your economic operations to a personal tax file.

The NIE is required to file almost any return

Without an NIE, you cannot file a modelo 100 (residents), modelo 210 (non-residents), modelo 720 (foreign assets), modelo 130 (autónomo), or any other return with the Agencia Tributaria. It is the identifier required on every form.

How is your tax status really determined in Spain?

Independent of the NIE, the Agencia Tributaria classifies every taxpayer in two categories: tax resident or non-tax resident. That qualification changes everything.

The three criteria for tax residency

Spain considers you a tax resident if you meet any of these criteria: you spend more than 183 days a year on Spanish territory (partial days count as full days); you have your centre of economic interests in Spain (business, main income source, primary assets); your spouse and minor children habitually reside in Spain (unless proven otherwise). Just one of the three suffices. For criteria details and examples, see how to become a tax resident in Spain.

If you are a tax resident

Spain taxes your worldwide income via the IRPF (progressive scale up to 47%). You file the modelo 100 every year between April and June for the previous year. You may also be required to file the modelo 720 declaring your foreign assets above €50,000. You do however gain access to bilateral tax treaties to avoid double taxation.

If you are not a tax resident

Spain only taxes your Spanish-source income via the IRNR (modelo 210). The rate is 19% for EU/EEA citizens and 24% for non-EU/EEA citizens. For a deep dive (renta imputada, rental, property sale), see how much tax you must pay as a non-resident in Spain.

What are the NIE's fiscal uses depending on your status?

The NIE serves different filings depending on whether you are a tax resident, non-resident, or in transition.

For a non-resident owner

The NIE is used to file the modelo 210 every year. If you do not use the property (second home), you pay on renta imputada (1.1% or 2% of the cadastral value, taxed at 19% EU or 24% non-EU). If you rent out the property, you pay on actual rents (with deductible expenses for EU/EEA citizens, no deduction for non-EU). The NIE appears on the modelo 210, on the IBI, and on the modelo 211 your buyer will file if you sell (3% withholding).

For a newly resident taxpayer

The NIE is used to file the annual modelo 100 and, if applicable, the modelo 720. If you become a tax resident mid-year (for example in June), you are resident for the entire fiscal year as soon as you exceed 183 days by December. That switch can trigger a retroactive IRPF obligation on all your income for the year. The mechanism is the same one explained in understanding fiscal vs social residence.

For an autónomo or SL director

The NIE is the main identifier of all your filings: modelo 130 (IRPF instalment), modelo 303 (IVA), modelo 100 (annual). For details, see how to become an autónomo in Spain and the step-by-step guide to setting up an SL. Note: the SL will have its own NIF (starting with B), distinct from your personal NIE. To understand the distinction, see the difference between NIE and NIF.

When does an NIE automatically trigger fiscal monitoring?

In some cases, the allocation of the NIE triggers automatic tax monitoring by the Agencia Tributaria.

On a property purchase

When you buy a property in Spain, the notary informs the Agencia Tributaria of the transaction. The tax office records you as an owner and expects a modelo 210 return from the following year if you are non-resident. Failure to file generates reminders and, eventually, sanctions.

On signing an employment contract

If a Spanish company hires you, your NIE appears on the contract and triggers registration with social security (NUSS). You are then presumed tax resident unless proven otherwise (for example A1 posting). The detail of the NUSS is in everything about the NUSS number in Spain.

On registering as autónomo

The RETA alta and the census alta with the Agencia Tributaria automatically place you in the active taxpayer status. Your quarterly obligations (modelo 303, 130) start immediately.

But without activity, the NIE stays passive

If you obtain an NIE and do nothing (no purchase, no rental, no employment contract), nothing happens fiscally. The Agencia Tributaria will not tax you "in anticipation". The NIE remains an inactive identifier until your first economic operation.

What are the most common NIE-related tax pitfalls?

Several mistakes recur and can cost you dearly.

Believing the NIE settles your tax status automatically

This is mistake number one. Holding an NIE and spending 200 days in Spain makes you a tax resident, regardless of any specific tax step. Conversely, holding an NIE without exceeding 183 days or having economic interests in Spain leaves you non-resident. To grasp these interactions properly, read the difference between fiscal and social residence. The myth is also dismantled in nine misconceptions about the NIE number.

Forgetting the modelo 210 as a non-resident owner

Owning an apartment without declaring it generates a tax debt every year (IRNR on renta imputada, generally €200-€800 per year depending on the cadastral value). After 4-5 undeclared years, the back tax + interest + fines can reach several thousand euros.

Forgetting the modelo 720 in year 1 of tax residency

If you become tax resident and you have foreign assets above €50,000 (bank accounts, securities, property), you must declare them via modelo 720 by 31 March. The historical minimum fine is €1,500, and it can be much heavier. Many expats discover this obligation after missing it.

Confusing personal NIE and company NIF

If you set up an SL, its NIF (starting with B) is distinct from your personal NIE. On invoices issued by the SL, that company NIF is what must appear. Mixing the two is a common error that complicates accounting and can generate tax adjustments.

Failing to plan the non-resident to resident switch

If you plan to become a tax resident, plan the year of the switch. Selling foreign assets, triggering dividends, or realising capital gains before becoming resident can save several thousand euros. This advice is even more crucial for expats with significant assets. A gestoría that knows both your home country and Spain is best placed to support you.

How does your NIE evolve with your tax status over time?

The NIE number is allocated for life and never changes. It is your tax status that evolves around it.

Phase 1: NIE allocated, non-resident status

You have your NIE but you live abroad and have no significant activity in Spain. You can file nothing, unless you own property (then annual modelo 210).

Phase 2: NIE and property

You buy an apartment. The NIE allows the Agencia Tributaria to track you. You file the modelo 210 every year. You pay the IBI to the town hall. No modelo 100 since you are not a tax resident.

Phase 3: NIE and settlement in Spain

You decide to settle permanently. You exceed 183 days, you become a tax resident. The same NIE is used to file the modelo 100 (worldwide income) and possibly the modelo 720 (foreign assets). You stop filing the modelo 210 since you are no longer non-resident.

Phase 4: NIE and economic activity

You open an activity (autónomo or SL). The NIE becomes the central identifier of all your professional filings. If you set up an SL, its company NIF complements your personal NIE.

Phase 5: Return abroad

You go back to live in your home country. Your NIE remains valid for life. If you keep a property in Spain, you become non-resident again and return to the modelo 210. The NIE has not changed.

In short: the NIE is a tool, not a status

The impact of the NIE on your tax status in Spain is neutral: it is an identifier that allows you to be tracked administratively but creates no obligation by itself. It is your economic operations (purchase, rental, sale, hire, activity) and your physical presence that determine what you pay to the Agencia Tributaria.

Good fiscal hygiene means clearly distinguishing three things: your identifier (NIE), your status (tax resident or non-resident), and your obligations (returns to file). These three dimensions interact but do not merge. Mastering this distinction avoids most nasty surprises and tax assessments. The full picture sits in everything about residency in Spain.

Want to take stock of your real tax status and the returns you should be filing? At gestoraz, we audit your situation, identify active or dormant obligations, and propose a compliance plan, especially if you have accumulated several years without filings or are preparing a status change.

Official sources

- Agencia Tributaria, tax residency, sede.agenciatributaria.gob.es: criteria and returns for residents and non-residents.

- Ley 35/2006 IRPF (BOE), boe.es/buscar/act.php?id=BOE-A-2006-20764: reference text on personal income tax.

- Real Decreto Legislativo 5/2004 IRNR (BOE), boe.es/buscar/act.php?id=BOE-A-2004-4527: reference text on non-resident income tax.

- Modelo 210 (instructions), sede.agenciatributaria.gob.es: non-resident return.

- Modelo 720 (instructions), sede.agenciatributaria.gob.es: declaration of foreign assets.

- Bilateral tax treaties, hacienda.gob.es: Spain-UK, Spain-France, Spain-Netherlands and others.

Obtain your Digital Certificate entirely remotely.

Request your Digital Certificate completely remotely.