What you need to know about taxes for a Sociedad Limitada

When we talk about taxes for a Sociedad Limitada in Spain, we enter a fiscal universe completely different from that of the autónomo. The SL is a legal entity in its own right: it has its own taxable profit, its own corporate income tax rate and its own filing calendar. Understanding how these taxes fit together is what separates a well-managed SL, optimising its taxation, from one paying 30% of avoidable taxes and accumulating fines for delays.

This article describes, in the order they intervene in the life of an SL, the four main taxes that apply: corporate income tax (IS), VAT (IVA), social charges linked to the director and employees, and IRPF that hits the director when they pay themselves in salary or dividend. Each time, we specify the rates, the modelos to file, the pitfalls to avoid, and above all how these taxes interact.

Why are SL taxes so different from those of an autónomo?

Before going into the detail of rates and modelos, you must understand why the SL and the autónomo do not play in the same fiscal world. This logic difference is what makes the SL more complex day-to-day, but also more interesting above a certain income level.

The SL is a separate legal entity

The autónomo is an individual: everything they invoice swells their personal income and goes through IRPF, the Spanish progressive scale that can rise to 47%. There is no wall between activity and person, fiscally, legally, economically it is the same entity.

The SL, conversely, is a legal entity created at the notary, registered with the Registro Mercantil and given its own fiscal identifier (NIF). It generates its own turnover, deducts its own costs, releases its own profit and pays its own tax, the Impuesto sobre Sociedades, at a flat rate. Partners and director remain legally separate from the company, which changes both the taxation and the liability.

Why double taxation is not always a trap

Many entrepreneurs see the SL as a double taxation system: money is taxed first in the company (IS), then again when it leaves to the director (IRPF on salary or dividend). On paper, that is correct. In practice, it is rarely a trap.

The Spanish IS rate (23% for most SLs, 15% in the first years) is significantly below the upper IRPF brackets (37%, 45%, 47%). For significant profits, the combination "23% IS + 19-23% on dividends" costs less than going directly through the IRPF progressive scale, especially when the director can modulate the share they actually take out of the company.

From what profit does the SL become more attractive?

The practical switch threshold sits around €50,000 to €60,000 of annual profit. Below, the SL's fixed costs (director's cuota at €350-€590/month, more expensive gestoría, heavier accounting, Annual Accounts filing) erode the fiscal advantage. Above, the combination of flat IS rate and choice between salary and dividend becomes clearly winning. To compare both statuses in detail, see autónomo vs SL in Spain and the step-by-step guide to setting up an SL.

What are the four main taxes that hit an SL?

Before getting into each tax, it helps to picture the whole. An SL is concerned with four big tax categories that do not all add up at the same moment or on the same base. Understanding which one weighs on what avoids nasty surprises when calculating the net result for the director.

Corporate income tax, the pivot of the system

The Impuesto sobre Sociedades (IS) is the heart of an SL's taxation. It applies on the company's profit once all costs are deducted, at a flat rate (23% most often, 15% in the first two profitable years). It is the corporate equivalent of IRPF, but without progressive scale, making it predictable and plannable.

IVA, a tax to manage rather than to pay

Spanish VAT (IVA) is not a cost for the SL itself: the company collects it on its sales on behalf of the state and deducts it from its purchases. The balance is paid to the Agencia Tributaria. But quarterly administrative management (modelo 303) requires rigour, and IVA weighs on cash flow between invoicing and remittance.

Social charges: employees and director

Social charges split into two blocks. On one side, employer contributions if the SL employs staff, around 30-35% of gross paid on top of the salary, often making it the heaviest tax when employing. On the other, the director's monthly cuota as autónomo societario, paid directly to the TGSS, which starts between €350 and €590/month with no access to the Tarifa Plana.

IRPF, which hits the money exit

Finally, IRPF intervenes when the director or partners take money out of the company. If they choose the salary, the IRPF progressive scale applies (up to 47%), and the SL withholds the tax at source via modelo 111. If they choose the dividend, the specific scale for capital income applies (19%, 21%, 23%, 27%, 28%). The choice between the two is the director's main fiscal optimisation lever.

How does corporate income tax (IS) work in Spain?

IS is the central tax of any SL and the first one fiscal planning focuses on. Its logic is simpler than IRPF, a single rate applied to profit, but its subtleties, especially on the reduced rate for young companies, deserve to be well understood.

What are the IS rates in force?

The rate depends essentially on the company's age and turnover.

| Situation | IS rate |

|---|---|

| Newly created SL, first profitable year + next | 15% |

| SL with turnover < €1,000,000 | 23% |

| SL with turnover ≥ €1,000,000 | 25% |

Most newly created SLs fall on the reduced 15% rate in the first two profitable years, then switch to 23% as long as they remain under the million-euro turnover bar.

Who can benefit from the 15% reduced rate?

The 15% reduced rate deserves particular attention, as it represents a significant saving during the start-up phase. It applies during two fiscal periods: the first in which the SL realises a profit, and the one immediately after.

The advantage is reserved for newly created entities, that is, SLs constituted from scratch and not from a transformation, split or contribution of pre-existing activity. The administration checks this in case of doubt, so it is useless to try to "rejuvenate" an existing activity by switching it into a new SL.

How to count the "first two profitable years"?

This is where the misunderstanding is most frequent. The rate does not apply during the first two calendar years of the SL's existence, but during the first two years where the company actually generates a positive fiscal profit.

Take an example. An SL created in 2025 records a loss of €5,000 in its first year. In 2026, it finally realises a profit of €20,000, then €40,000 in 2027. The reduced rate counter only triggers from 2026, the first profitable year. The 15% rate then applies to fiscal years 2026 and 2027, so €3,000 of IS in the first profitable year and €6,000 in the next. From 2028, the standard 23% rate takes over. Over the two years where the reduced rate applied, the saving is €3,200 compared to the standard rate, which is far from negligible for a young structure.

How is the fiscal profit of an SL calculated?

IS applies on fiscal profit, not turnover. Understanding how this profit is calculated is therefore the first reflex of good management: it is here that both legitimate optimisations and the most costly errors lodge.

The basic formula

The calculation follows simple logic on paper but requires rigorous accounting in practice:

fiscal profit = turnover − deductible costs − depreciation − provisions − prior losses

It is this fiscal profit, not turnover, not gross accounting profit, that serves as the IS base.

Which costs are deductible in an SL?

Where the SL takes the advantage over the autónomo is in the perimeter of deductible costs. An SL can deduct practically everything that serves the economic activity, without the grey zones to which the autónomo is regularly faced when working from home or using their personal vehicle.

Concretely, this covers gross salaries paid to employees and employer contributions, office rent and charges (electricity, water, internet), professional equipment via depreciation (computers, furniture, machines), professional travel and accommodation expenses, marketing and advertising spend, notary, lawyer and gestoría fees, plus professional insurance, banking fees and loan interest.

The point is therefore not to invent costs, but to rigorously document everything legitimately deductible. A good gestoría can often identify €5,000 to €10,000 of forgotten costs per year on growing SLs.

Why loss carry-forward is an under-rated asset

A point that many young SLs forget: losses from prior fiscal years can be carried forward without time limit on future profits. Concretely, an SL losing €30,000 in its first two years can erase those €30,000 of future profit as soon as it starts being profitable, saving €6,900 of IS at the standard rate.

It is a fiscal advantage that is lost only if you ignore it: it must be explicitly carried forward in the modelo 200 every year. Failing to do so is essentially handing this money over to the state.

When and how do you declare corporate income tax?

Knowing the rate is not enough: you still have to file the right modelos at the right dates. Spain combines an annual return and quarterly instalments that can trap an inattentive SL.

Modelo 200, the annual July return

The annual IS return is filed via the modelo 200, in July for the previous fiscal year (SLs generally use the calendar year, so July 2026 for fiscal year 2025). It is in this modelo that the definitive profit is calculated, the rate is applied and the regularisation is made against instalments already paid.

Quarterly instalments via modelo 202

The Spanish tax administration does not just wait for the annual return: it also requires quarterly instalments via the modelo 202, filed in April, October and December. These instalments are calculated on estimated profit for the current year and are deducted from the final IS.

What happens in case of delay?

Forgetting an instalment does not just trigger late interest: it can also compromise the possibility of opting for some special regimes and alert the tax inspection. Better to schedule these dates in a dedicated calendar, and it is one of the first tasks a gestoría externalises for its SL clients.

How does IVA apply to an SL?

IVA is the tax that demands the most administrative discipline from an SL, even though it does not weigh on its results. Its logic is different from IS: the SL is not its economic taxpayer, but its collector on behalf of the state.

Why IVA is not a cost for the SL

IVA (Spanish VAT, general rate of 21%) is not a tax economically weighing on the SL itself: the company collects it on its sales on behalf of the state, and deducts it on its purchases. The balance, IVA collected minus IVA deductible, is paid to the Agencia Tributaria. So it is above all an administratively managed tax, but the SL bears the cash flow burden between invoicing (and advancing the IVA collected) and remittance.

The three modelos to know: 303, 390, 349

The three returns to know are: the modelo 303 is quarterly (April, July, October, January) and summarises IVA collected and deductible for the quarter. The modelo 390 is the annual summary, filed at end of January for the previous year. Finally, the modelo 349 concerns intra-EU operations: if your SL sells or buys services and goods in other EU countries, it must declare those flows separately.

The IVA advantage of an SL over an autónomo

Compared to an autónomo, an SL typically has more deductible IVA, premises, equipment, professional services, software subscriptions, which reduces the balance to pay. It is not a direct fiscal advantage, but it improves cash flow and partially compensates for additional administrative costs. To check which rate applies to your own products or services, see check which VAT rate applies in 2025.

How much do social charges cost for an SL?

Social charges are often the most underestimated tax when setting up an SL. They can exceed the IS itself when the company employs staff or the director takes a substantial salary.

Employer and employee contributions for staff

For employees, the employer (the SL) pays an employer contribution of about 30 to 35% of gross salary, funding social security, unemployment and professional training. The employee bears an employee contribution of about 6.35% withheld on their gross. To this is added the IRPF withholding at source, declared monthly via the modelo 111 and summarised annually via the modelo 190.

To grasp the system as a whole, see how the Spanish social security system works for self-employed and businesses.

The director's cuota: why it costs more than a standard autónomo

For the director (administrador) of the SL, the situation is particular: they must register with social security as an autónomo societario and pay their own monthly cuota directly to the TGSS. This cuota starts directly between €350 and €590/month depending on the declared income tramo, representing between €4,200 and €7,080 a year to factor into the company budget.

Why the Tarifa Plana does not apply to directors

Bad news for new directors: unlike standard autónomos who can benefit from the Tarifa Plana at €80/month for the first twelve months, SL directors are not entitled to it. The Spanish legislator considers that the SL director already benefits from the legal advantage of a legal entity and fiscal optimisation via dividends, so they do not need the social boost. It is a fixed expense to anticipate from the first month of activity. The detail of the underlying social system sits in everything about the NUSS number.

Salary or dividend: how do you pay yourself in an SL?

This is probably the most asked question by new SL directors, and it has no universal answer. The right choice depends on the profit level, the director's personal situation and their cash flow needs.

The salary option (nómina): simple and deductible

The salary option consists of paying yourself a monthly salary like any employee. On the SL side, the salary is a deductible charge that reduces the IS taxable profit. On the director's side, the salary is taxed at IRPF on the progressive scale (up to 47%) and the SL withholds the IRPF at source via the modelo 111.

It is the simplest option to account for, and it has the advantage of regularly feeding the director's personal cash flow. It is also more reassuring for a director who wishes to clearly separate professional and personal life.

The dividend option: double taxation but a softer scale

The dividend option is different: the profit is first taxed by IS at 23% (or 15% if the SL is still on the reduced rate), then what remains can be distributed to partners as a dividend. The dividend is then taxed in the shareholder's IRPF, but on a specific scale for capital income, much softer than the general scale: 19% up to €6,000, 21% between €6,001 and €50,000, 23% between €50,001 and €200,000, 27% between €200,001 and €300,000, and 28% beyond.

The total cost is therefore indeed double taxation (IS + IRPF), but the combined rate often remains below the marginal IRPF rate that an equivalent autónomo would have suffered.

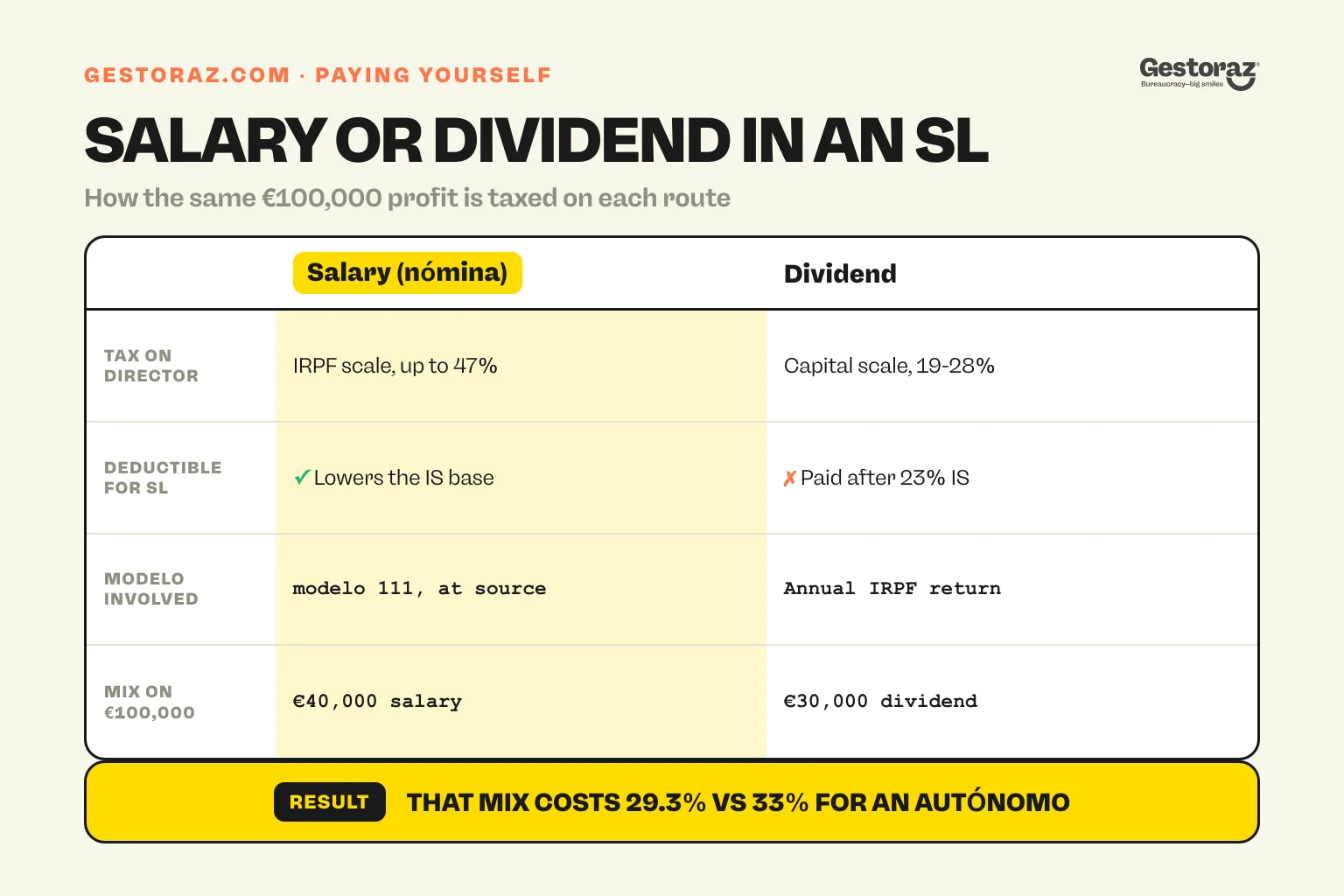

Combined example on €100,000 of profit

Take a combined example illustrating the trade-off. An SL realises €100,000 of profit. The director chooses to take €40,000 in salary and to distribute €30,000 in dividend.

The €40,000 salary is deductible on the SL side, bringing the IS base down to €60,000, so an IS of €13,800 (23%). The €30,000 dividend is then taxed in the director's IRPF at about 20% on average, so €6,000. Finally, the director's IRPF on the €40,000 salary is about €9,500. Total combined: €29,300, an effective rate of 29.3% on the €100,000 of initial profit.

For comparison, an autónomo who had generated the same €100,000 profit would pay about €33,000 of IRPF, so 33% effective. Above €100,000 of profit, the gap widens further in favour of the SL; below €30,000, the autónomo often remains more advantageous because of the SL's fixed costs.

What other administrative obligations apply to an SL?

Beyond taxes proper, an SL is subject to several administrative obligations that can generate heavy fines if forgotten. These are often the first points checked in case of an audit.

Filing the Annual Accounts at the Registro Mercantil

Filing the Annual Accounts (Cuentas Anuales) with the Registro Mercantil is mandatory each year, generally in July. Delay or absence of filing triggers fines from €1,200 to €60,000 depending on company size, plus a registry block preventing any official act, manager change, capital increase, share transfer. It is a formality you never have an interest in postponing.

IAE and the million-euro threshold

The Impuesto sobre Actividades Económicas (IAE) applies to SLs whose turnover exceeds €1,000,000. Below this threshold, the SL is exempt but must still register with the IAE to declare its activity code. It is a purely declarative step when you do not reach the threshold, but omission can generate administrative penalties.

Modelo 232 on related-party transactions

The modelo 232 concerns transactions between related parties, for example, loans between the SL and its director, or invoicing to another company in the same group, above a certain amount. It is one of the favourite control points of the tax inspection, as it often reveals borderline optimisation schemes.

What is the typical total annual cost of an SL?

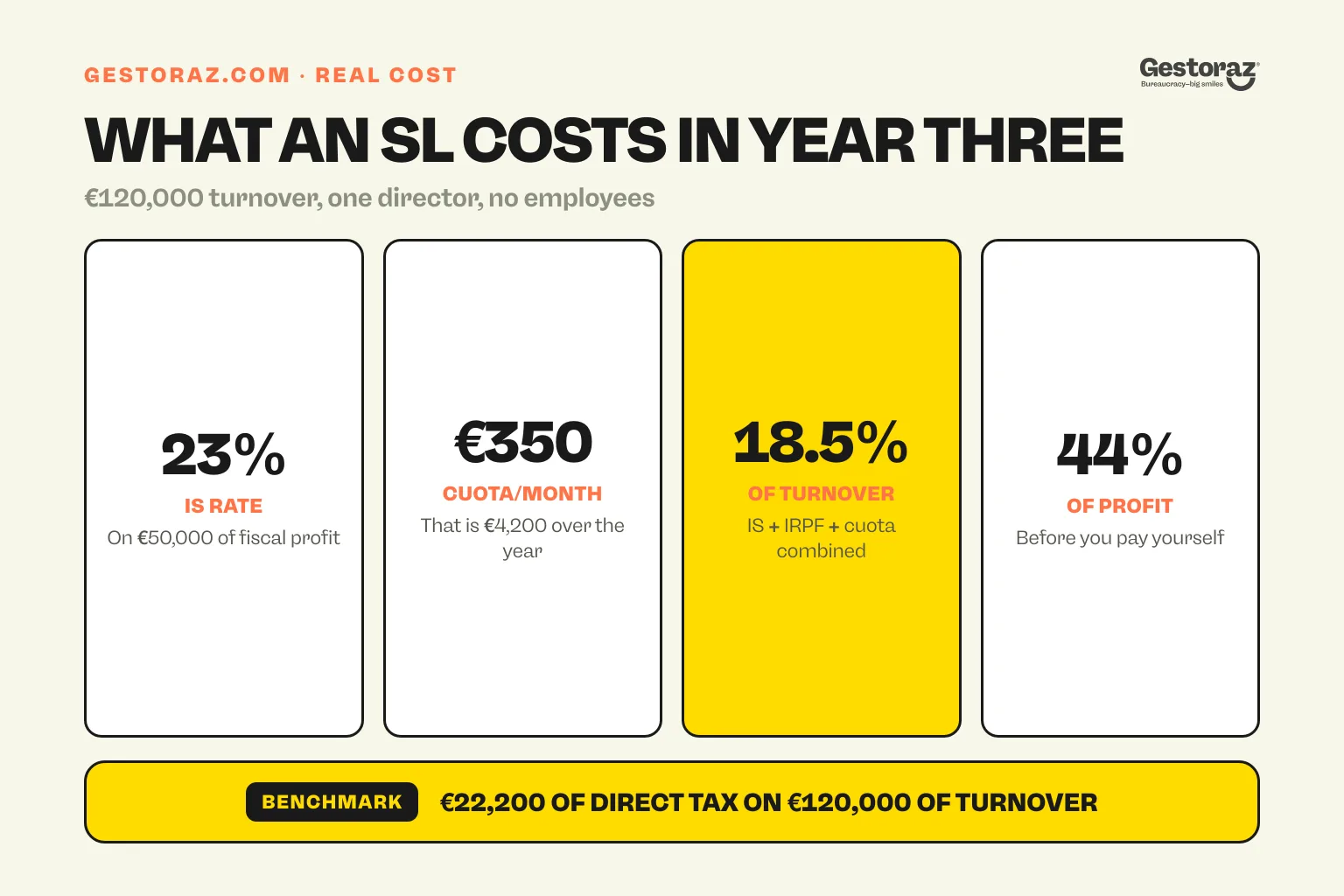

To make all this tangible, take a concrete example of an SL in its third year, with realistic assumptions for a sole director without employees.

Example assumptions

The SL is in its third year (so no longer at the 15% reduced rate), with €120,000 of turnover, €40,000 of deductible costs excluding director compensation, and a director paying themselves €30,000 of annual salary. No employees, no complex intra-EU operations.

Tax-by-tax breakdown

The taxable profit is calculated starting from turnover, so €120,000 − €40,000 of costs − €30,000 of director's salary (which is itself a deductible cost) = €50,000 of fiscal profit. The IS applied at 23% gives €11,500.

To this is added the director's IRPF on the €30,000 salary, about €6,500 according to the scale, allowances included. The administrator's monthly cuota is €350 × 12 = €4,200 over the year. VAT is not a net cost but requires cash flow throughout the year. Finally, the fees of a specialised gestoría typically cost €200 to €350/month and are fully deductible, so €2,400 to €4,200/year.

Effective taxation ratio

In total, direct taxation (IS + IRPF + cuota) on this example reaches €22,200, about 18.5% of turnover, or 44% of the initial fiscal profit before director compensation. It is a useful benchmark to calibrate expectations when creating an SL and compare it to the effective rate of an equivalent autónomo, which would rather be around 27-30%.

What mistakes should you absolutely avoid?

Three or four mistakes recur in almost every SL in difficulty file. Knowing them avoids both heavy fines and tax audits.

The director who forgets their cuota

The most costly error, by far, is the director who forgets or refuses to pay their autónomo societario cuota. The TGSS always catches up eventually, often with two years of contributions + interest + penalties at once, which can represent €8,000 to €15,000 to settle in one shot. It is not a theoretical case: it is a classic pattern with foreign founders who think their director status suffices.

The misunderstanding on the "first two years"

On the 15% reduced rate, the most frequent confusion is to believe it applies during the first two calendar years of the SL. The exact rule is that it applies during the first two profitable years, a detail that changes everything for an SL that starts slowly, and that can lose several thousand euros of tax saving if applied wrongly in the modelo 200.

Late Annual Accounts and badly carried losses

Late Annual Accounts trigger immediate fines and an administrative block complicating any subsequent notarial deed. Many directors also forget to carry forward losses correctly from prior years, losing a fiscal advantage they had legitimately earned. Finally, modelo 232 is regularly neglected, even though it is on the priority list of tax inspection control points.

Should you take the leap towards an SL?

The taxes for a Sociedad Limitada in Spain form a more complex system than the autónomo's, but one that becomes significantly more advantageous as soon as the annual profit exceeds €50,000 to €60,000. The 15% reduced IS rate in the first two profitable years, the broad cost deductibility, and the salary-dividend trade-off offer real optimisation levers that the autónomo does not have.

The trade-off is administrative: annual modelo 200, quarterly modelo 202, modelo 303 and 390 for VAT, modelo 111 and 190 for withholdings, plus the Annual Accounts and director's cuota. For many directors, delegating to a specialised SL gestoría costs €200-€350/month but avoids dozens of hours of administrative work and several thousand euros of potential fines. The full set-up path sits in the step-by-step guide to setting up an SL and the comparison with the alternative is in autónomo vs SL in Spain.

Are you considering setting up an SL or migrating from autónomo status? At gestoraz, we can precisely quantify the threshold above which switching to an SL becomes profitable for your activity, and then manage the entire annual fiscal cycle.

Official sources

- Agencia Tributaria, sede.agenciatributaria.gob.es: all fiscal modelos (200, 202, 303, 390, 111, 190, 232).

- Ley 27/2014 del Impuesto sobre Sociedades (BOE), boe.es/buscar/act.php?id=BOE-A-2014-12328: reference text on IS, 15% reduced rate, loss carry-forward.

- Ley 37/1992 del IVA (BOE), boe.es/buscar/act.php?id=BOE-A-1992-28740: reference text for Spanish VAT.

- Tesorería General de la Seguridad Social (TGSS), sede.seg-social.gob.es: SL alta as employer, director's cuota as autónomo societario, CCC codes.

- Registro Mercantil Central, rmc.es: filing of Annual Accounts (Cuentas Anuales).

- Colegio de Registradores, registradores.org: practical information on accounts filing and legal publicity.

Obtain your Digital Certificate entirely remotely.

Request your Digital Certificate completely remotely.