How much tax must I pay as a non-resident in Spain?

The non-resident tax in Spain surprises many foreign owners who think that having a holiday home in Spain is limited to paying the property tax (IBI) and the water bill. The reality is different: as soon as you own a property, rent it out, or sell it, you fall under the IRNR (Impuesto sobre la Renta de no Residentes) managed by the Agencia Tributaria. This tax applies automatically and forgetting it generates back tax with penalties over 4 years.

This article explains exactly when you are considered a non-resident in Spain, which taxes apply in the three main scenarios (ownership without rental, rental, sale), how the taxable bases are calculated, which forms to file and on what dates, and which mistakes save you from nasty surprises during an audit.

When are you considered a non-resident in Spain?

Before calculating the taxes, you must clarify your status. You are a non-resident if you meet none of the three tax residency criteria.

The three tax residency criteria (NOT to meet)

You are not a tax resident if you spend less than 183 days a year in Spain, your main economic interests are abroad, and your spouse and minor children do not habitually reside in Spain. If you meet one of these criteria, you become a tax resident and this article no longer concerns you. For details, see how to become a tax resident in Spain.

The three main scenarios for a non-resident

As a non-resident, Spain only taxes you on your Spanish-source income. Three scenarios cover 95% of cases: ownership of a property without rental (renta imputada), rental of a property (actual income), and sale of a property (capital gain). Each has its own rules, forms and calendars.

EU/EEA vs non-EU/EEA differences

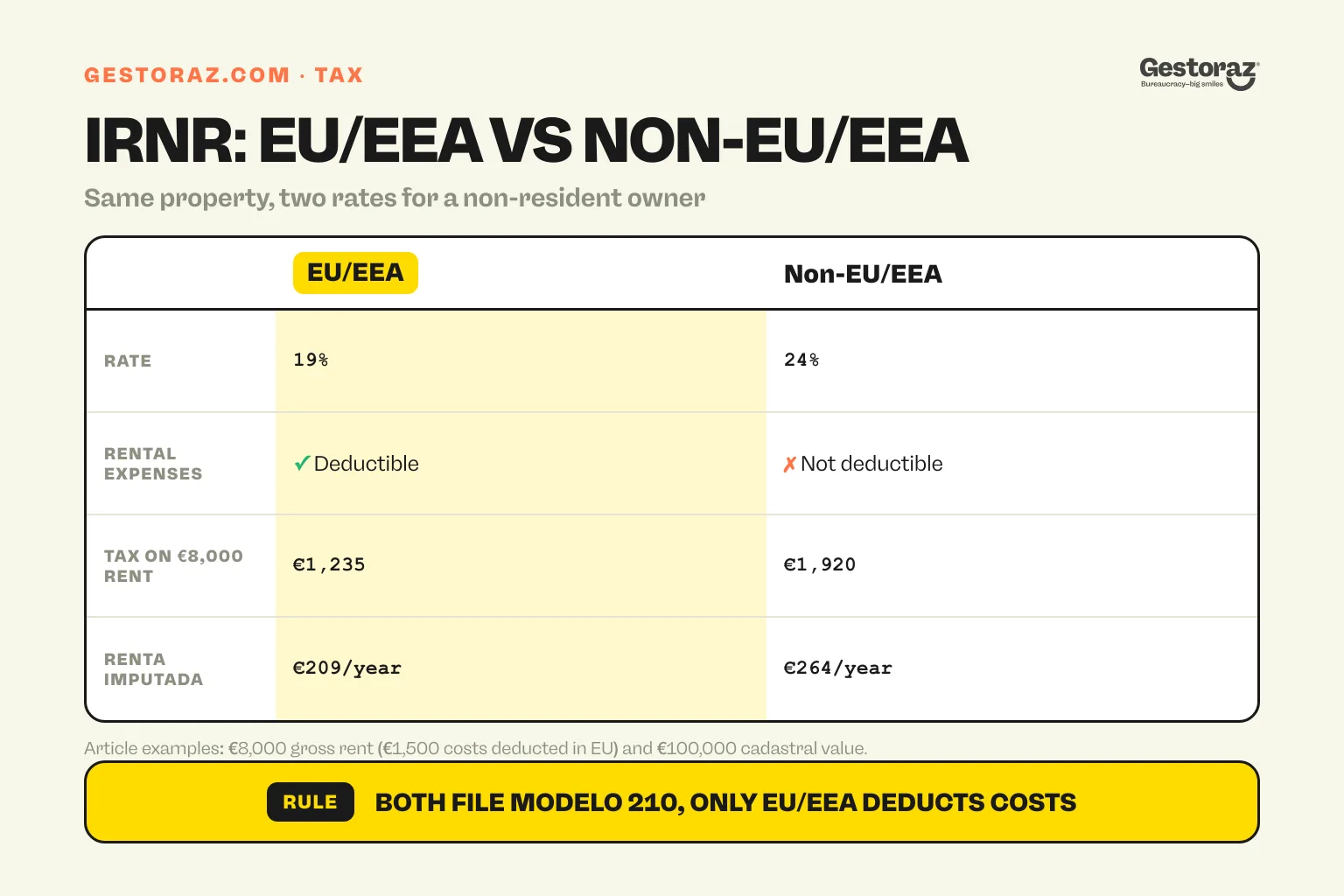

Spain applies different rates and rules depending on your nationality. EU/EEA citizens (France, Belgium, Germany, Netherlands, Italy, Norway, Iceland, etc.) benefit from lower rates (19%) and the possibility of deducting expenses on rental income. Non-EU/EEA citizens (British since Brexit, Swiss, American, Moroccan, etc.) are taxed at 24% without expense deduction. This difference can represent thousands of euros a year for an active property investor.

Scenario 1: ownership without rental (renta imputada)

This is the typical case of the holiday home owner in Spain. Even without renting, you pay an imputed tax on the supposed "use value" of the property.

The renta imputada principle

Spain considers that owning a property without renting it generates a fictitious income (renta imputada) corresponding to personal use or rental potential. This fictitious income is calculated as a percentage of the cadastral value (valor catastral, indicated on the annual IBI).

The calculation

- 1.1% of the cadastral value if the property has been the subject of a cadastral revision in the last 10 years.

- 2% of the cadastral value otherwise.

The fictitious income is then taxed at 19% (EU/EEA) or 24% (non-EU/EEA).

Worked example

Take an apartment in Alicante with a cadastral value of €100,000 revised in 2018. The fictitious income is: 1.1% × €100,000 = €1,100. The tax for a French citizen (EU) is: 19% × €1,100 = €209/year. For a British citizen (non-EU post-Brexit), the tax is: 24% × €1,100 = €264/year.

Filing: annual modelo 210

You file the modelo 210 every year before 31 December for the current year. You can file it yourself via the Agencia Tributaria sede electrónica (with a digital certificate or Cl@ve) or delegate to a gestoría.

Scenario 2: rental of a property (actual income)

If you rent out your property as long-term or holiday let, you are taxed on the actual rents received, plus the standard IBI municipal tax.

For EU/EEA citizens: deduction of expenses

You declare gross rents received then deduct expenses directly linked to the rental: management fees (gestoría, platform), maintenance work, mortgage interest, IBI, communal taxes, insurance, depreciation (3% of the acquisition value excluding land). The net income obtained is taxed at 19%.

For non-EU/EEA citizens: no deduction

You pay 24% on gross rents, with no expense deduction. This is significantly more punitive. This Brexit difference particularly hit British property owners in Spain.

Worked example for an EU resident

A French owner rents out his apartment in Marbella for 4 months as a holiday let for €8,000 in gross rents. He deducts €1,500 of expenses (gestoría €600, IBI €400, insurance €200, interest €200, depreciation €100). Net income: €8,000 − €1,500 = €6,500. Tax: 19% × €6,500 = €1,235.

Example for a non-EU resident

The same case for a Swiss citizen: tax on €8,000 gross at 24% = €1,920. That is €685 more for the same rents.

Filing: quarterly modelo 210

For rental income, the modelo 210 must be filed quarterly within 20 days following the end of each quarter (April, July, October, January). If you rent out year-round, you file 4 modelos per year.

SES Hospedajes obligation

Since December 2024, short-term holiday lets must register their travellers on the SES Hospedajes platform of the Ministry of the Interior. See register at SES Hospedajes and mandatory rental registration in Spain.

Scenario 3: sale of a property (capital gain)

When you sell a property, Spain taxes the realised capital gain at a flat rate.

Capital gain calculation

Capital gain = (sale price − sale fees) − acquisition value. The acquisition value includes the price originally paid, notarial fees, transfer duties (ITP/AJD), and any improvement work. Sale fees include agency commissions, energy certificates, etc.

Applicable rate

The rate is 19% for EU/EEA citizens and 24% for non-EU/EEA citizens, with no distinction by holding period (unlike some countries).

The 3% withholding by the buyer

At the time of sale, the buyer withholds 3% of the sale price and pays it directly to the Agencia Tributaria via the modelo 211. It is an advance on your capital gains tax. You then recover the difference (if the advance exceeds the tax due) or pay the balance (if it is insufficient).

Worked example

A Belgian sells an apartment in Valencia bought in 2014 for €180,000 (with €15,000 of acquisition fees, so an acquisition value of €195,000). He sells in 2026 for €260,000 with €15,000 of sale fees (agency commission). Capital gain: (€260,000 − €15,000) − €195,000 = €50,000. Tax: 19% × €50,000 = €9,500. The 3% withholding by the buyer was 3% × €260,000 = €7,800. Balance to pay by the seller: €9,500 − €7,800 = €1,700.

Filing: modelo 210 within 4 months

The capital gain return is filed via a specific modelo 210, within 4 months of signing the sale deed. Missing this window generates significant penalties.

What other obligations apply to a non-resident owner?

Beyond the IRNR, several other taxes and administrative obligations apply.

IBI (Impuesto sobre Bienes Inmuebles)

The IBI is the municipal property tax, paid every year to the town hall of the municipality where the property is located. The rate varies by municipality (between 0.4% and 1.3% of the cadastral value). It is a tax distinct from the IRNR: you pay both, not one or the other.

Basura and other local taxes

Municipal taxes for rubbish collection (basura), water and other services can reach €200-€500/year depending on the municipality. They are paid separately from the IRNR and the IBI.

Wealth tax (Impuesto sobre el Patrimonio)

Some autonomous communities (Catalonia, Madrid with recent exemption, Valencian Community) apply a wealth tax for non-residents with high property assets in Spain. The triggering threshold varies (generally from €700,000-€1,000,000 of Spanish assets).

Inheritance and gift tax

If you transfer the property to your heirs or make a gift, the Spanish inheritance and gift tax applies on the Spanish part of the estate. The scales vary widely by autonomous community (Andalusia almost exempt, Catalonia more expensive).

How can you avoid involuntarily switching to tax resident status?

If you want to remain a non-resident, watch the switch criteria.

Keep a precise calendar of presence days

Systematically note your dates of arrival and departure from Spain. At 183 days, you switch automatically. Many owners underestimate their presence (especially with partial days counted as full days) and find themselves tax residents without knowing.

Keep your centre of economic interests abroad

If you move your main activity (job, business) to Spain, you can become a tax resident even without exceeding 183 days. To remain a non-resident, keep your professional activity in your country of origin.

Document your situation

In case of an audit, the Agencia Tributaria can requalify your status. Keep proof of your life abroad (electricity bills for the main home, plane tickets, employment contracts, tax returns from the country of origin). These documents are the best defence in case of dispute.

Understand the impact on your status

Holding an NIE does not make you a tax resident. To grasp this nuance properly, see the impact of your NIE on your tax status and everything about residency in Spain.

What mistakes are common for non-resident owners?

Several mistakes recur and can cost thousands of euros.

Believing the IBI covers everything

Mistake number one: thinking that paying the IBI is enough to be in order. The IBI is the equivalent of municipal property tax; the IRNR (modelo 210) is a distinct national tax. Both are due each year.

Forgetting the modelo 210 on renta imputada

Many non-resident owners do not declare the renta imputada because they do not use the property. This is a mistake: the modelo 210 is mandatory even without use. Failing to file generates back tax over 4 years plus penalties.

Wrong calculation of acquisition value at sale

When selling, forgetting to include notarial fees, ITP, and improvements in the acquisition value artificially inflates the capital gain and therefore the tax. Keep all invoices since the purchase.

Filing the modelo 210 late

For rentals, the 20-day quarterly deadline is strict. For sales, 4 months after the deed. Late filing generates penalties even if the amount due is small.

Confusing EU and non-EU regimes

A British post-Brexit owner who continues to apply the 19% rate and EU deductions is in breach. Check your fiscal nationality at the time of each return.

Failing to appoint a fiscal representative

For non-residents who do not master the sede electrónica, appointing a fiscal representative (gestoría) in Spain is almost essential to meet the calendars. Without a representative, Agencia Tributaria notifications can be missed.

What does a non-resident owner's tax year really cost?

Here are some ranges to calibrate your budget.

For an apartment of €200,000 cadastral value (EU)

- Annual IBI: €800.

- Renta imputada: 19% × 1.1% × €200,000 = €418.

- Basura, water, communal: €800-€2,000.

- Gestoría fees (modelo 210): €100-€150 if only this modelo.

- Annual total: €2,100-€3,400.

For an apartment rented out 4 months (EU)

- Same costs as above, plus rental income tax (variable).

- For €8,000 of gross rents with €1,500 of deductible expenses: €1,235 of rental IRNR.

- Annual total: ~€3,500-€4,700.

For the same situation in non-EU

- No expense deduction on rents: 24% × €8,000 = €1,920 of IRNR.

- Renta imputada: 24% × 1.1% × €200,000 = €528.

- Annual extra cost vs EU: ~€700-€1,000.

Where to start with your non-resident taxes in Spain

The non-resident tax in Spain is not optional: the Agencia Tributaria actively checks non-filings thanks to data from notaries, property registers, and rental platforms. The three main scenarios (ownership, rental, sale) each have their own forms and calendars, and the EU/non-EU difference can represent thousands of euros a year.

The practical rule: file the modelo 210 on renta imputada every year before 31 December, the quarterly modelo 210 on rents if you rent, and the specific modelo 210 within 4 months of a sale. Keep all invoices (purchase, work, sale) so you can justify the calculations in case of an audit. The wider context of residency types is in everything about residency in Spain and the social side is in understanding fiscal vs social residence.

Do you have a property in Spain and are not sure you have declared everything correctly? At gestoraz, we can audit your fiscal history, file the necessary regularisations, and manage the annual or quarterly returns for €100-€300 a year depending on complexity.

Official sources

- Agencia Tributaria, modelo 210, sede.agenciatributaria.gob.es: non-resident return and instructions by scenario.

- Real Decreto Legislativo 5/2004 (IRNR) (BOE), boe.es/buscar/act.php?id=BOE-A-2004-4527: reference text on non-resident income tax.

- Modelo 211 (instructions), sede.agenciatributaria.gob.es: 3% withholding on property sale.

- Catastro Inmobiliario, catastro.minhap.gob.es: consultation of cadastral values.

- Spain-UK tax treaty, hacienda.gob.es: post-Brexit status for British citizens.

- Spain-France tax treaty, hacienda.gob.es: avoiding double taxation between France and Spain.

- Real Decreto 1776/2004 (BOE), boe.es/buscar/act.php?id=BOE-A-2004-13957: IRNR implementing regulation.

Obtain your Digital Certificate entirely remotely.

Request your Digital Certificate completely remotely.